Africa’s Food Import Reliance Set to Deepen

The halting reopening of the Strait of Hormuz will fail to mitigate systemic risks mounting across the agribusiness supply chain - leaving low-income economies disproportionately exposed.

The OECD and FAO’s latest Agricultural Outlook 2026-2035, released on 29 June, points to slowing demand growth and sharply rising production costs for the 2026-27 harvest. The fallout is being felt most acutely in low-income countries, most of them in Africa.

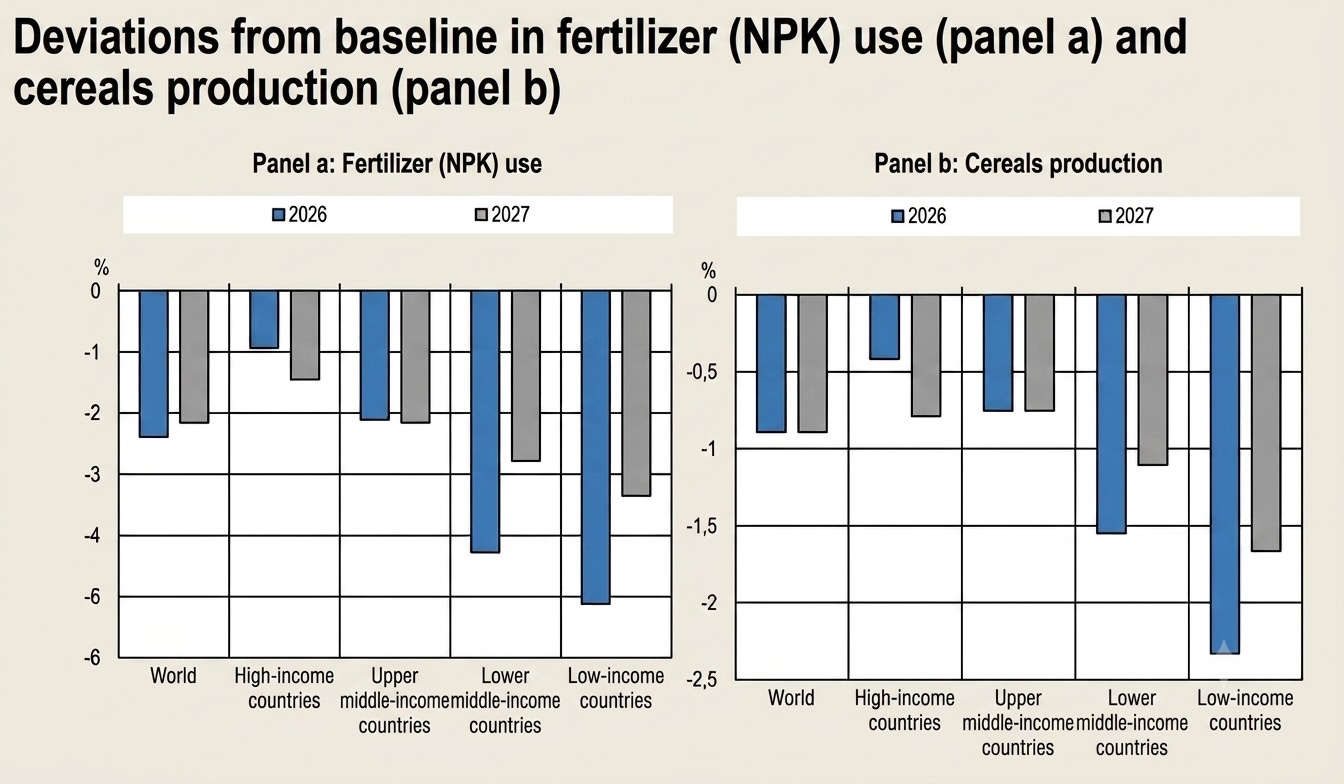

Fertilizer prices spiked as soon as the Middle East conflict broke out: nitrogen fertilizers rose between 30 and 50%, while urea prices were up 45% year-on-year by May 2026. Coming just ahead of the planting season, the surge forced farmers to scale back purchases “markedly in both low‑income countries (5.1% in 2026 and 3.4% in 2027) and lower middle‑income countries (4.3% and 2.8%),” the OECD notes.

Further reading : OECD-FAO Agricultural Outlook, June 2026

These forced cutbacks will weigh heavily on the next harvest’s yields. Global grain output is projected to fall 0.9% in the 2026-27 season. “The downturn will be sharper in low-income countries, where a 1.7% decline is expected,” says Marion Jansen, Director of the OECD’s Trade and Agriculture Directorate. It bears noting that Africa already ranks among the world’s lowest fertilizer users: farmers in Uganda or Madagascar apply as little as 2 to 3 kg of fertilizer per hectare, against a global average of 135 kg.

Budgetary constraints

Faced with this external shock, governments’ capacity to mount a domestic response is immediately constrained by the state of public finances. In Senegal, with a debt-to-GDP ratio of roughly 132% and a budget deficit above 5% in 2026, President Bassirou Diomaye Faye’s government has very little fiscal room to manoeuvre. While the government managed to mobilize a 130 billion FCFA package (nearly $216 million) on June 30 - over half of which is earmarked for fertilizer procurement - it has also had to announce a partial clearance of a pre-existing 154 billion FCFA debt (over $256 million) owed to input suppliers simply to unlock stalled supply chains.

Crisis management is proving equally perilous in Ghana. Classified as a lower-middle-income country, it is only just emerging from its 2022 sovereign default, under a strict IMF-mandated fiscal consolidation programme.

Populations caught in the squeeze

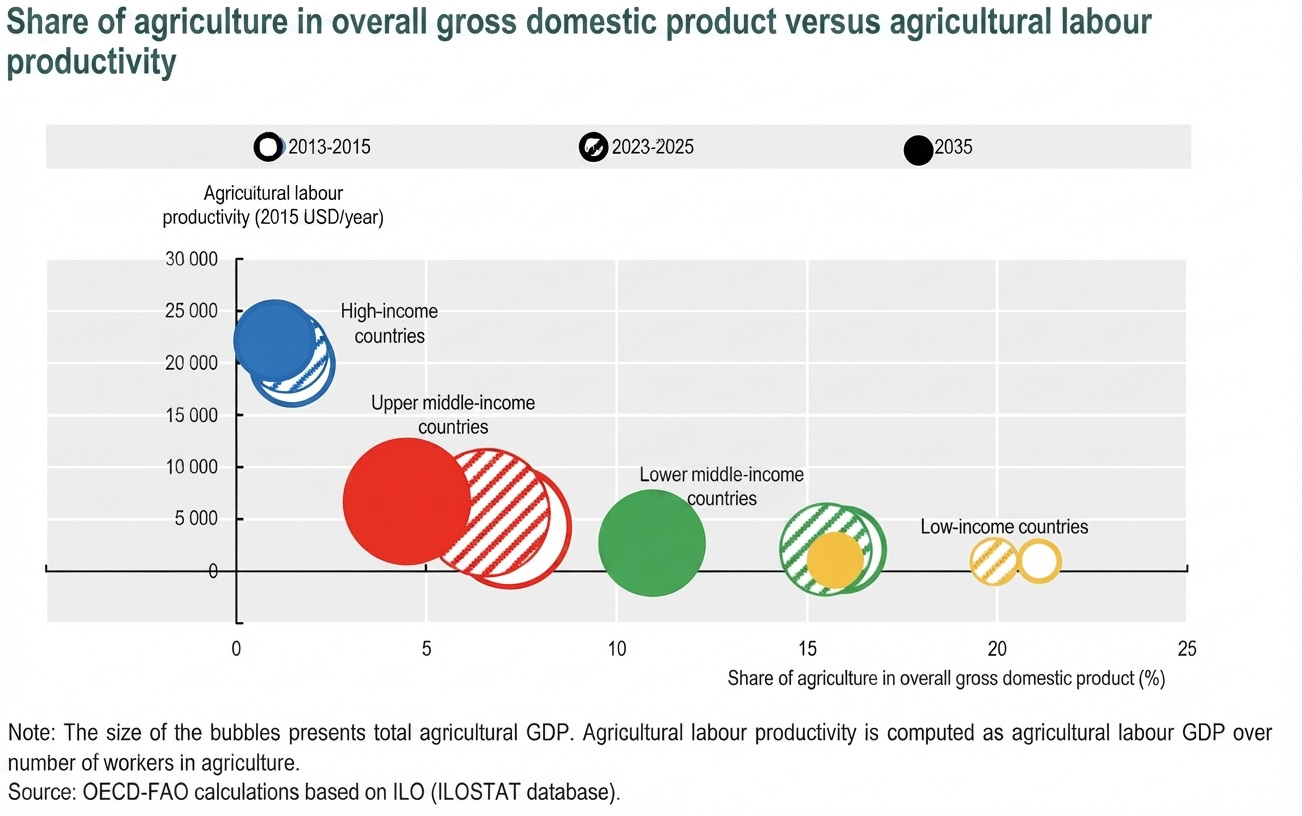

In economies where agriculture accounts for 15 to 20% of GDP, large segments of the population already live with chronic food insecurity. UN Secretary-General António Guterres sounded the alarm in the Global Report on Food Crises, published in April 2026: “The recent escalation of conflict in the Middle East is disrupting trade routes, driving up food and fuel prices, and destabilizing populations, potentially exacerbating hunger,” he wrote.

West and Central Africa face a crisis with multiple, compounding causes. Data from IFPRI (the International Food Policy Research Institute) show that the 41.8 million people already in acute food crisis at the end of 2025 are projected to swell to 52.8 million between June and August 2026.

Further reading: “The State of Food Security and Nutrition in the World 2025”, FAO, July 2025

In Ghana, the World Food Programme’s latest analysis puts the number of people facing “crisis-level” food insecurity this summer at 1.5 million, or 4% of the population. This aggregate figure masks stark disparities, with vulnerability climbing to 8% among rural women. In Senegal, while the share of the population at risk of acute food insecurity remains contained (around 2 to 3%, according to the FAO), that population has grown 47% year-on-year - a troubling trajectory.

Compounding this squeeze, regional governments are confronting a sharp drawdown in multilateral assistance. Over the past year, the WFP’s global operational funding plummeted by 40%, dropping from $10 billion to $6.4 billion. This shortfall is a direct consequence of a budgetary retrenchment by the United States, whose contribution was slashed from approximately $7 billion to $3 billion.

A slow-burning, delayed-onset crisis

The OECD-FAO report remains fundamentally conservative in its baseline projections, choosing to classify these trends as “vulnerabilities“ rather than an active food crisis. Because its market projections are built on the prior year’s data, the report does not fully capture immediate climate risks. Yet the El Niño episode taking shape for the second half of 2026 could act as a major risk multiplier: according to the FAO, more than 80% of drought-related agricultural shocks are expected to hit low- and middle-income nations.

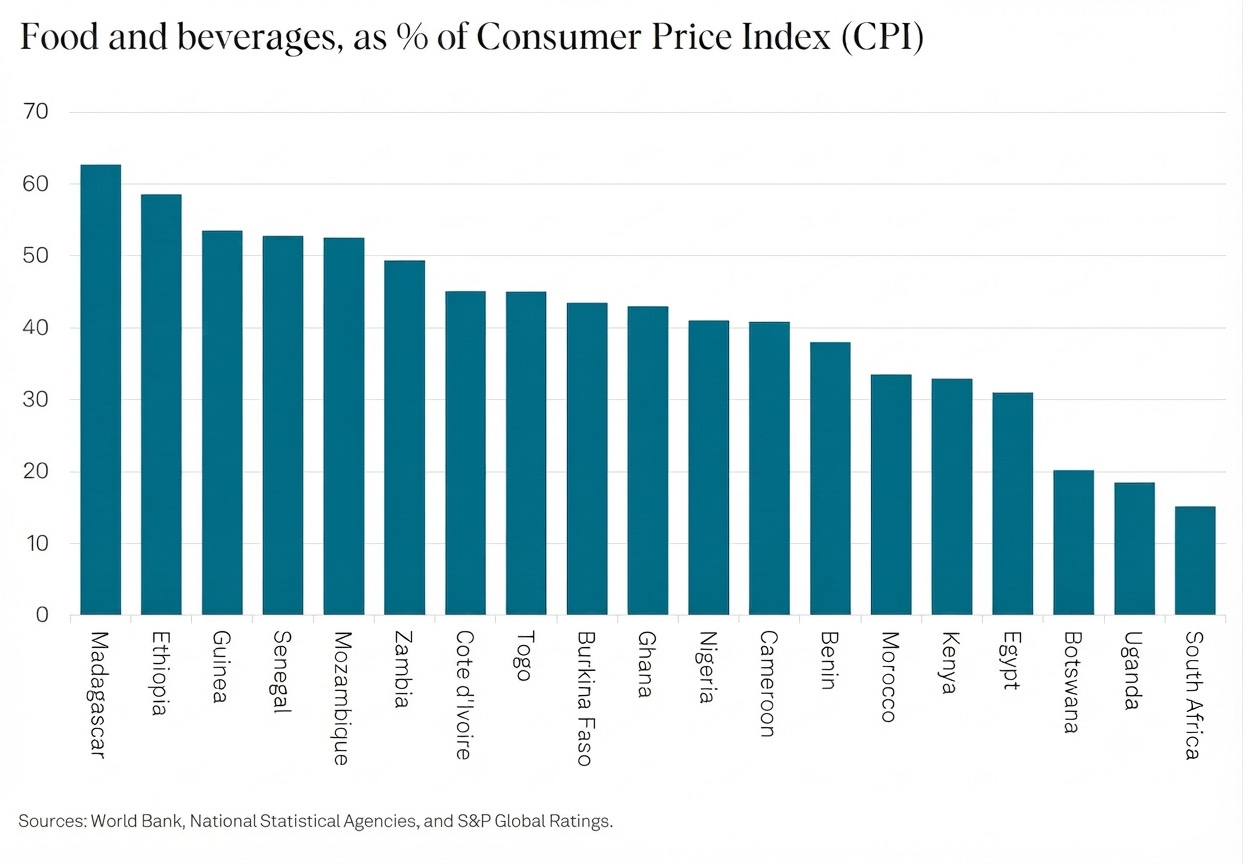

At minimum, households in the most fragile economies — where food spending often exceeds 40% of disposable income — will be forced to downgrade their diets, favouring cereals over animal protein.

However, the full macro-to-micro transmission has yet to peak. “Fertilizer price pressures reach CPI with a six- to 18-month delay. Pass-through from increased transportation costs to food prices is very likely to be faster,“ S&P Global warned in a note1.

A durable, structural dependency

Beyond the immediate cyclical shock, the OECD identifies deep-seated structural bottlenecks: inadequate transport networks, limited storage capacity, and weak trade facilitation systems - “all of which increase transaction costs and reduce competitiveness.“

Driven by the combined effect of robust demographic growth (projected at 25% to 30% over the next decade) alongside rigid domestic production ceilings, food imports are forecasted to surge by 55% in Sub-Saharan Africa and by 34% in the Middle East and North Africa (MENA) region by 2035. Absent investments and political reforms to build greater self-sufficiency, these regions will remain structurally exposed to the volatility of global commodity markets.

“African Markets Highlights - Global Energy Shock Tests Resilience”, June 2026